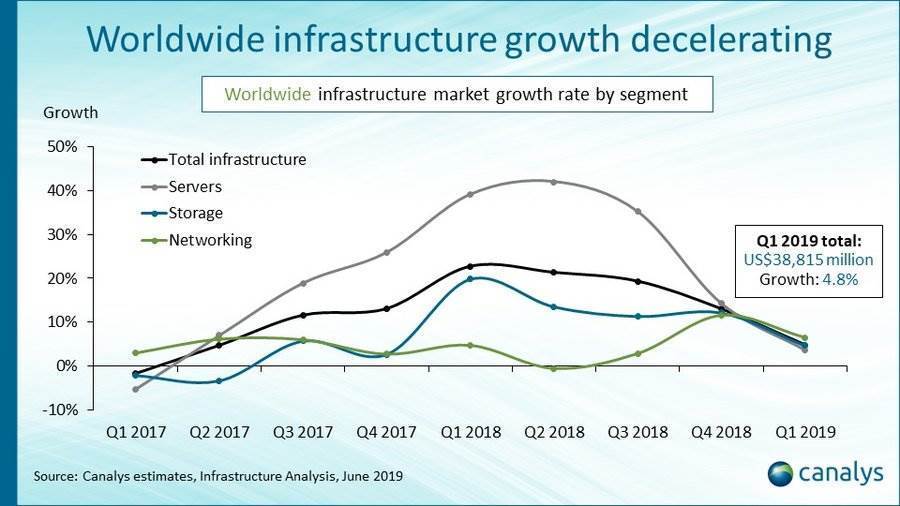

The global market for data centre infrastructure has stalled, according to analyst outfit Canalys.

The firm’s new latest look at shipments of servers, storage and networking infrastructure found that growth in Q1 2019 was 4.8 percent, a decent number but rather less than full year 2018’s growth rate of 16.3 percent.

Canalys blamed the dip on “A marked slowdown in capital expenditure by the hyperscale cloud builders, combined with ongoing weakness in service provider spending, the end of the mainframe refresh cycle, and smaller expansion in enterprise server and storage sales”. But that still made for total shipment US$1.8 billion higher than the same period in 2019.

Networking was the only infrastructure segment to register stronger growth than last year, albeit at a relatively low level, increasing 6.5 percent. Refresh of campus networks and the debut of WiFi 6 helped things along. SD WAN also drove sales.

Servers hurt the most in Q1. Shipments grew 3.7 percent, but that was much less than Q1 2018’s 39.2 percent growth.

Cisco, Dell EMC and HPE rule these markets, collectively scooping 52.1 percent of total shipments, a smidgen up from 50.5 percent a year ago.

Canalys said “Cisco continued to dominate each segment of the networking market, while Dell EMC made further gains in the channel in both servers and storage. HPE remained the leading challenger in all segments, with its Aruba wireless LAN business taking further share.” Huawei scored fourth place with 7.3 percent market share, but Canalys said “It is arguably facing the biggest supply chain challenges among any of the top four vendors, given the US Executive Order signed on 15 May.

And the firm worried that geopolitics could hurt the entire market, writing that “the outlook for the rest of the year is uncertain, as the fallout from escalating trade disputes starts to affect global trade and economic performance.”

.jpg&h=142&w=230&c=1&s=1)

.jpg&h=142&w=230&c=1&s=1)

.jpg&w=100&c=1&s=0)

.jpg&w=100&c=1&s=0)