IDC has released research that shows the semiconductor market is expected to stabilise by mid-2022, potentially reaching overcapacity in 2023.

As larger-scale capacity expansion come online toward the end of 2022, production could outpace demand.

The chip shortage has had wide-ranging ramifications, with several companies stating it has impacted their bottom line for FY21. Intel previously said it could last years and TSMC, among others, raising prices.

The statement from IDC reflects research from Gartner earlier this year stating the shortage would ease by the mid-2022.

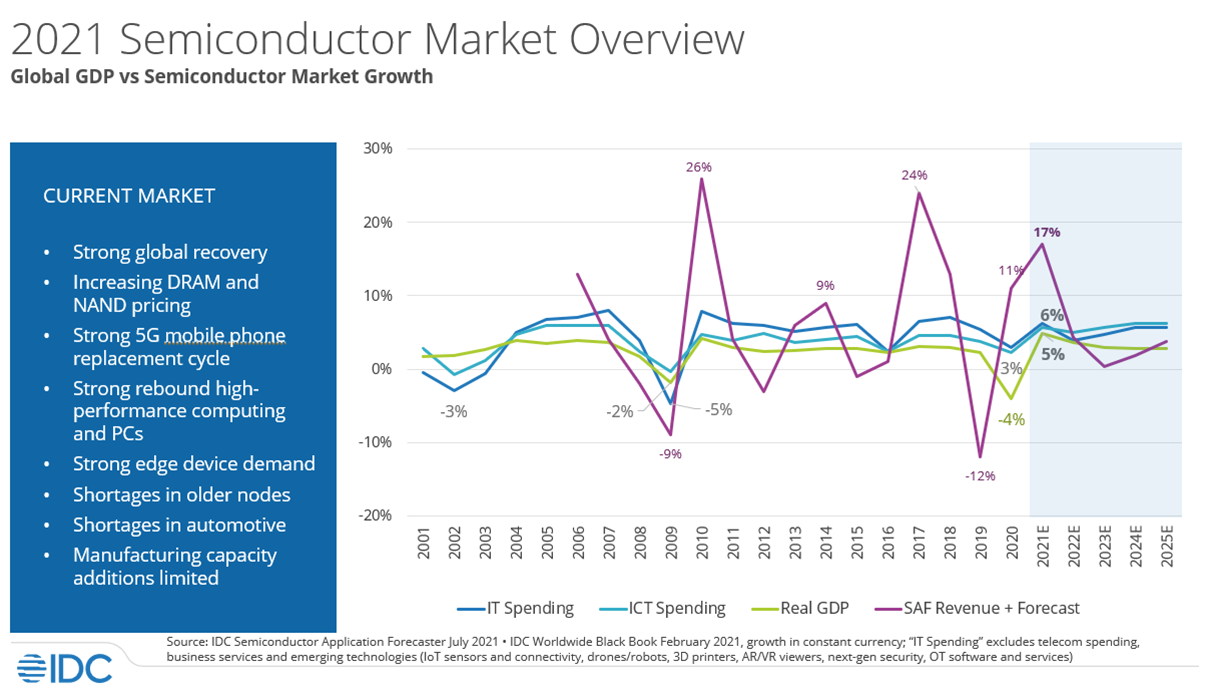

In terms of demand, IDC said that the 2021 market is expected to grow by 17.3 percent in 2021, exceeding the 10.8 percent growth in 2020.

It also predicted that the global semiconductor market will see a high 5.3 percent CAGR to reach US$600 billion by 2025.

This growth is driven by mobile phones, notebooks, servers, automotive, smart home, gaming, wearables, and Wi-Fi access points.

Integrated circuit (IC) shortages should also ease toward the end of 2021 due to accelerated capacity additions.

“The semiconductor content story is intact and not only does it benefit the semiconductor companies, but the unit volume growth in many of the markets that they serve will also continue to drive very good growth for the semiconductor market,” said IDC enabling technologies and semiconductors group vice president Mario Morales in the release.

IDC reported that front-end manufacturing is starting to meet demand in the third quarter of 2021 thanks to dedicated foundries working with fabless suppliers. However, it added that “larger issues and shortages” mean back-end shortages will continue.

The company also provided more detail into the semiconductor market growth areas.

5G semiconductor revenues will increase by 128 percent, with total mobile phone semiconductors expected to grow by 28.5 percent.

Growth will also be strong for game consoles (34 percent), smart home (20 percent), and wearables (21 percent).

The automotive semiconductor shortage should be sorted by the end of the year, with revenues increasing by 22.8 percent.

Notebook semiconductor revenues will grow by 11.8 percent, while X86 Server semi revenues will increase by 24.6 percent.

The rising costs of semiconductor wafers will be maintained throughout 2021 thanks to material costs and opportunity cost in mature process technologies, the company said.

.jpeg&h=142&w=230&c=1&s=1)

.jpg&w=100&c=1&s=0)

.jpg&w=100&c=1&s=0)

.jpg&w=100&c=1&s=0)