Research firms Gartner and Canalys have revealed that the ongoing semiconductor shortage has contributed to the global PC market’s relatively stagnant growth, echoing research from IDC released yesterday.

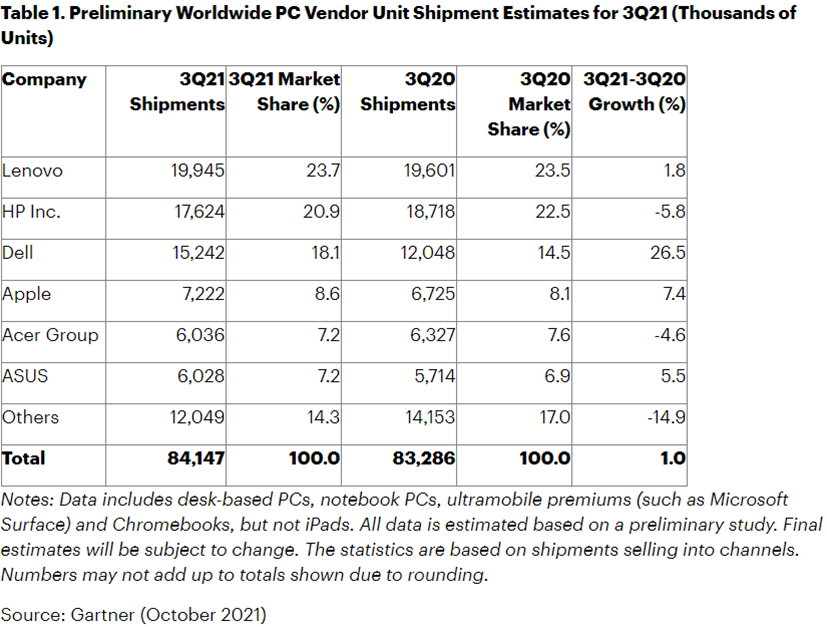

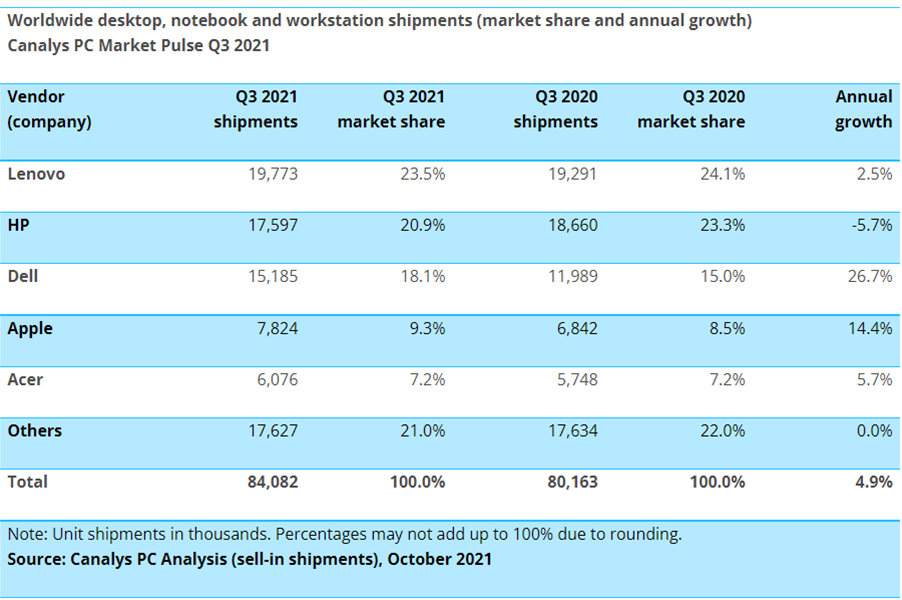

Gartner said worldwide PC shipments in Q3 2021 increased 1 percent to 84.1 million year over year, while Canalys found it grew 5 percent also at 84.1 million units. The numbers both include Chromebooks, which Canalys had always done and a first for Gartner for the sector.

Both of their research cited the semiconductor shortage as a factor for the slowed growth, following several consecutive quarters of double digit increases, but also cited other factors that have dampened demand.

Gartner’s research found consumer and educational spending began to shift away from PCs to other priorities like COVID-19 vaccines, which had been more widely available during the period.

“As many schools worldwide reopened, there was no longer an immediate need for PCs and Chromebooks to support at-home education,” Gartner research director Mikako Kitagawa said.

“Business PC demand remained strong, led by economic recovery in key regions and the return of some workers to offices,” she added.

“However, business PC growth was concentrated in the desktop segment as semiconductor shortages continued to constrain laptop shipments. These component shortages are expected to persist into the first half of 2022.”

Gartner noted Chromebook shipments saw a 17 percent decline due to decreased demand in the education market, saying it was also the first time the segment posted a double-digit year-over-year decline in Chromebook sales since its introduction to the market in 2011.

Canalys meanwhile painted a bleaker picture, calling supply and logistics “deteriorating” as both vendors and channel partners both struggled to fulfill orders as backlogs persist.

Canalys senior analyst Ishan Dutt said, “Disruption to the global supply chain and logistics network remains the key inhibitor of higher growth in the PC market.”

“More than a year on from the onset of the pandemic, manufacturing continues to be hindered by lockdowns and other COVID-19 related restrictions, particularly in Asia. This has been compounded by a massive slowdown in global transportation with freight prices and delay times skyrocketing as a number of industries compete to meet unfulfilled demand.”

Dutt added that supply issues will go well into 2022 and expects the holiday season will see a significant portion of orders not met.

“Vendors able to manage this period of operational upheaval by diversifying production and distribution and having better visibility of orders to prioritize device allocation will be equipped to ride out the storm,” he said.

On a per-vendor basis, both Canalys and Gartner reported double-digit growth from Dell and Apple, while HP's shipments dropped. Lenovo still retains the top spot despite remaining steady.

Both said Asia-Pacific (excluding Japan) specifically saw increases during the period, with Gartner reporting 5.7 percent year over year growth for the region and Canalys reporting 13 percent growth.

Gartner said the growth comes as the region has “returned normal” despite the impact of the COVID-19 Delta variant.

Looking ahead, Gartner said the global rollout of Microsoft Windows 11 in Q4 2021 is expected to have a limited immediate impact for the business market as enterprise-class PCs will likely continue to be available with Windows 10 until 2023. The firm predicts less than 10 percent of new enterprise PCs will be deployed with Windows 11 by early 2023.

.jpg&h=142&w=230&c=1&s=1)

.jpeg&h=142&w=230&c=1&s=1)

.jpg&w=100&c=1&s=0)

.jpg&w=100&c=1&s=0)

.jpg&w=100&c=1&s=0)